Start Up Loan

Start Up LoanWhat borrowers in this group experienced

This is not a vague concern about poor communication. This is a specific pattern: a borrower who took active steps to meet their obligations, set up a direct debit in good faith, and then had years of silence — no statements, no arrears notices, no contact — before receiving unexpected correspondence in 2025.

If this is your situation, you are in the right place.

Two specific things to look out for

Did you receive a backdated regulatory letter dated December 2024?

Some borrowers in this cohort received regulatory letters in late 2024 or early 2025 that were backdated — issued as though they related to activity from an earlier period. This appears to have been GC Business Finance's attempt to regularise accounts that had received no contact for years. If you received correspondence with a date that did not match when you actually received it, note this carefully.

Did you receive an email about "State Aid" or a State Aid figure (such as a euro amount)?

Some borrowers received an email referencing a "State Aid" figure — often denominated in euros. This email may have been connected to Covid-era support schemes and could have been interpreted as the loan having been written off or absorbed into a support package. It was not. If you received such an email and believed as a result that your loan had been resolved or written off, this misunderstanding may be highly relevant to your complaint. Keep this email if you have it, and request it via SAR if you do not.

Why the direct debit matters

Setting up a direct debit is a clear, documented act of intent to repay. It is not the behaviour of someone trying to avoid their obligations — it is the opposite.

If a direct debit was in place and payments were not being collected, the question of who knew what, and when, becomes significant. A borrower cannot be expected to chase a lender that has gone silent, particularly if they had no reason to believe anything was wrong.

Key questions your SAR response should answer:

- Was the direct debit recorded as active on the account?

- Were any payments collected — and if not, when did collections stop and why?

- What contact attempts, if any, were made between 2020 and 2025?

- When was any default notice issued, and by what method was it sent?

- At what point was any default registered with credit reference agencies?

- Was any email sent referencing "State Aid" in connection with the account — and if so, what was the purpose and intended meaning of that communication?

- When were any regulatory letters issued, and if they carry dates that predate their actual dispatch, what is the explanation for that?

What "remediation" means in this context

In financial services, a remediation project is an internal process a firm undertakes when it has identified that a group of customers may have been affected by a process failure or error.

The fact that GC Business Finance has written to borrowers about a remediation project is significant. It suggests the firm has already identified, internally, that something may not have been handled correctly for a specific cohort of accounts — and that your account may be one of them.

You are not simply a dissatisfied customer. If you received a remediation letter, you are part of a group the lender itself has flagged as potentially affected. That changes the nature of any complaint or challenge you make.

Remediation is not automatic compensation. Firms often conduct these reviews quietly and offer the minimum unless borrowers engage formally, ask direct questions, and push for specific outcomes. The steps below explain how to do that.

What to do if this is your situation

-

Submit a Subject Access Request immediately.

This is your legal right under UK GDPR and it is free. Ask for everything — all account notes, contact records, direct debit records, internal flags, and any record of when and how any default was registered. GC Business Finance must respond within 30 days. Use the SAR template.

-

Keep the remediation letter and note all reference numbers.

Store it safely and make a copy. Any project reference or case number mentioned will be needed in all future correspondence.

-

Check your credit file at all three agencies.

Check Experian, Equifax, and TransUnion (all three can differ). Note the exact date any default was registered. This is free at each agency. If a default was registered without a prior default notice, or during a period when your direct debit was supposedly active, that is significant.

-

Respond to the remediation letter in writing.

Do not ignore it. Write back formally, confirm you have received it, state that you are engaging with the process, and ask for a clear explanation of: what the project covers, what GC has identified went wrong, what outcome they are proposing for your account, and the timeline for resolution.

-

Make a formal complaint if you are not satisfied.

Use the formal complaint template. State the direct debit was in place, that you received no contact for the period in question, and set out clearly what outcome you are seeking — whether that is removal of a default, an explanation, or redress for harm caused.

-

Use the timeline builder to document your case.

A dated chronology of events — loan date, direct debit setup, last contact received, date of remediation letter — is one of the most effective tools in any complaint. Build yours here.

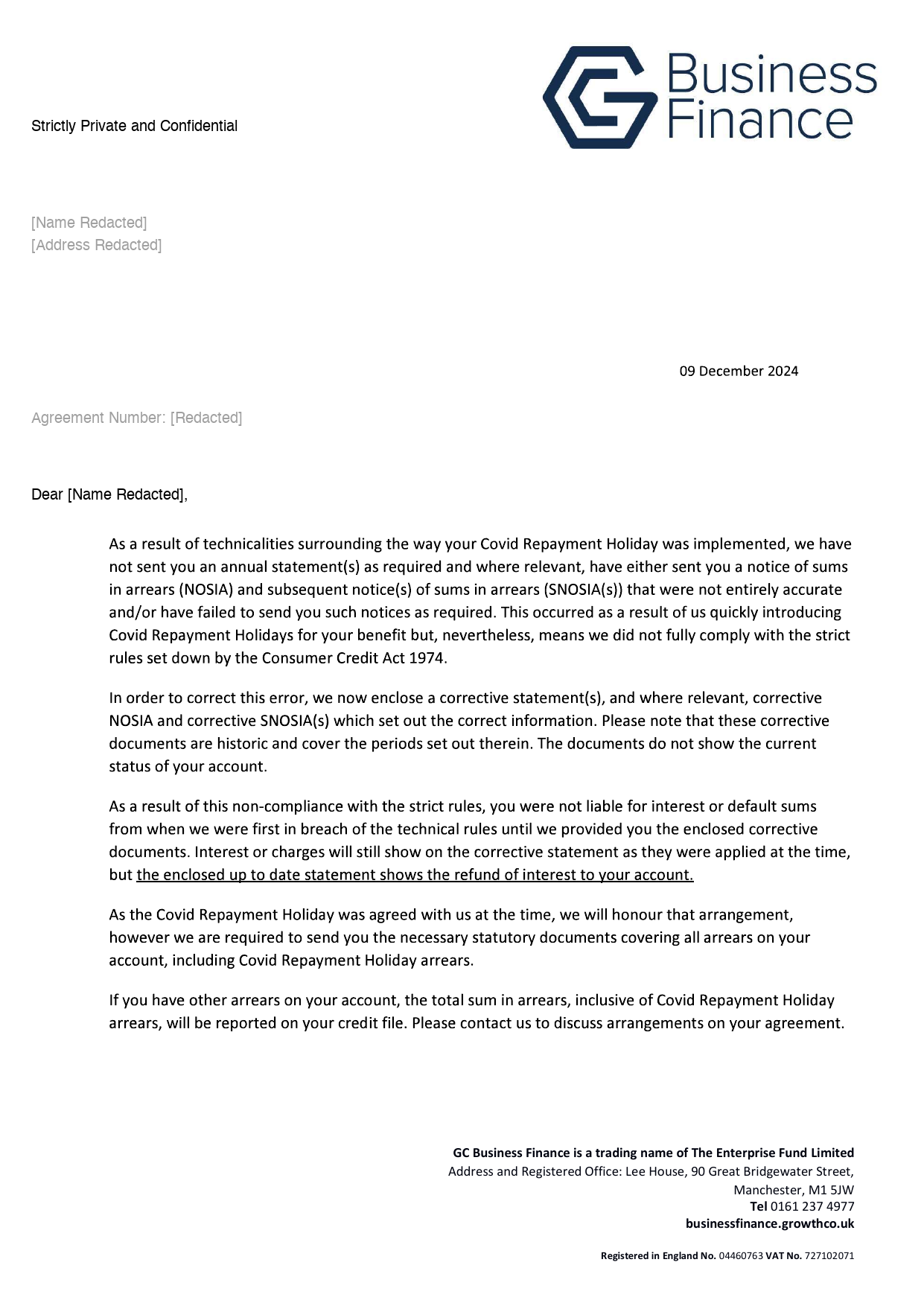

What GC Business Finance's own letter admits

In December 2024, GC Business Finance wrote to affected borrowers. The letter — a copy of which is shown below with personal details removed — contains significant admissions. These are GC's own words:

GC admits it failed to comply with the Consumer Credit Act 1974:

"means we did not fully comply with the strict rules set down by the Consumer Credit Act 1974."

GC admits it failed to send required annual statements: "we have not sent you an annual statement(s) as required."

GC admits it sent incorrect or missing Notices of Sums in Arrears: "have either sent you a notice of sums in arrears (NOSIA)... that were not entirely accurate and/or have failed to send you such notices as required."

GC confirms interest was not owed during the period of non-compliance: "you were not liable for interest or default sums from when we were first in breach of the technical rules until we provided you the enclosed corrective documents."

GC frames this as a "technicality" arising from how Covid Repayment Holidays were implemented. But the effect was that borrowers went years without the regulatory documents they were legally entitled to — annual statements and accurate arrears notices — which the Consumer Credit Act requires specifically so that borrowers can understand and manage their accounts.

The letter also states that the corrective statements enclosed are historic and "do not show the current status of your account." A separate up-to-date statement showing the refund of interest was enclosed. If you received this letter and did not also receive a separate current statement, request one.

The letter — redacted copy

Personal details have been removed. The letter text and enclosed statement are reproduced in full. Click any page to view at full size.

The two organisations involved

Start Up Loans Company

Issues the loans and sets the programme terms. Part of the British Business Bank.

startuploans.co.uk ↗GC Business Finance

Administers loan accounts as a delivery partner. The organisation from which remediation correspondence has been received.

businessfinance.growthco.uk ↗Is this your situation?

If you took out a loan around 2020, had a direct debit in place, and received no meaningful contact until 2025 — please share your experience. Every response helps establish how widespread this pattern is and supports the case for fair outcomes for everyone affected.

Share Your Experience Anonymously →